Equity release hits all-time high

An unprecedented 82,791 UK homeowners released equity from their property wealth during 2018, according to year-end market figures from sector trade body the Equity Release Council.

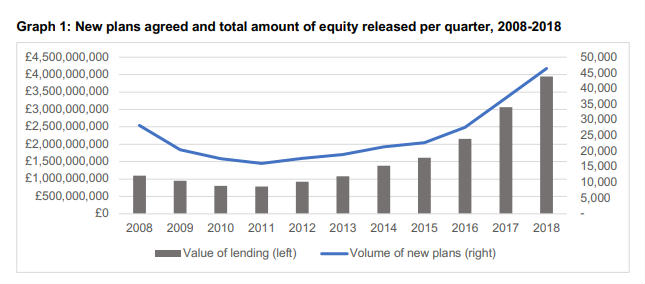

A record Q4 meant saw 12,891 new equity release plans agreed between October and December, contributing to an annual total of 46,397 people opting for the process for the first time.

Both these figures represent new highs and increases of 25 per cent year-on-year, as more consumers look to wealth built up in property to support their finances beyond the age of 55.

Total lending activity for 2018 grew for a seventh consecutive year to reach £3.94bn, up 29 per cent year-on-year, with £1.08bn of housing wealth unlocked in the final three months of the year. This was the most activity seen to date on either a quarterly or annual basis.

The figures show how unlocking property wealth via equity release has become an integral option within later life financial planning. Older homeowners collectively drew on £136 of housing wealth every second during Q4 2018: almost matching the current full new state pension weekly allowance of £164.

The 46,397 new plans agreed in 2018 via Council members were more than double the 22,749 seen three years ago in 2015, and four times the 11,484 seen over the course of the 1990s when consumer-focused industry standards were first established.

These standards continue to ensure that today’s customers benefit from clear and robust product safeguards and independent legal advice, alongside regulated financial advice when considering whether releasing property wealth is a suitable option to meet their needs.

Growth in the popularity of equity release products has been fuelled by a wide range of new product features and flexibilities appearing on the market.

Growth in the popularity of equity release products has been fuelled by a wide range of new product features and flexibilities appearing on the market. As of August 2018, 139 product options were available to consumers, more than double the number (58) seen two years ago in 2016 and up from 24 in 2007.

These include:

- options to receive regular monthly income from housing wealth to boost other sources

of retirement funds, such as the state pension and private pension savings - options to pay interest each month (rather than rolling up interest) with no risk of default

- options to make voluntary capital repayments free from early repayment charges

- flexibilities for customers wising to downsize in future or guarantee a minimum

inheritance to leave behind.

While the customer base has grown to new levels, with further growth expected to help meet social needs, the average amounts withdrawn by homeowners have remained steady as customers release equity in moderation to fulfil their financial needs.

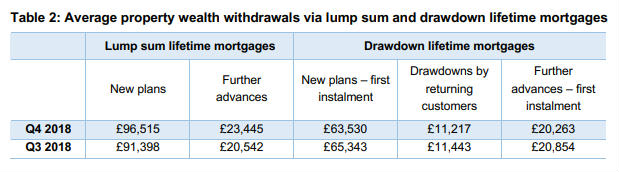

During Q4 2018, the first instalment of a drawdown lifetime mortgage was £63,530, compared to £62,359 a year earlier – a sum equivalent to 7½ years of state pension support. The average new lump sum lifetime mortgage in Q4 was £96,515, down from £101,913 in Q4 2017 and equivalent to more than 11 years of state pension support.

Drawdown products were chosen by 65 per cent of new customers during Q4 while 35 per cent opted for lump sum products.

David Burrowes, chairman of the Equity Release Council, said: “The equity release market continues to experience sustained growth as it proves a vital tool for consumers looking to make the most of their financial resources in later life. Older homeowners are realising in growing numbers that property wealth can play a crucial role in supporting their retirement alongside pensions, savings and other assets.

“Industry, regulators and government must continue to explore how we can help generations of retirees, both today and in the future, to adopt a more rounded approach to later life planning.

“With a growing choice of products and features on offer, the market is maturing and adapting to offer a new level of flexibility to suit a range of financial needs and ambitions – from funding care costs to helping children to buy their first home. Equity release now plays a pivotal social role and the Equity Release Council will continue to ensure that products are underpinned by robust consumer safeguards.”