RBS: Scottish private sector hit by September slowdown

Scotland’s private sector experienced a decline in September, with output falling for the first time since January, according to Royal Bank of Scotland’s (RBS) latest PMI survey.

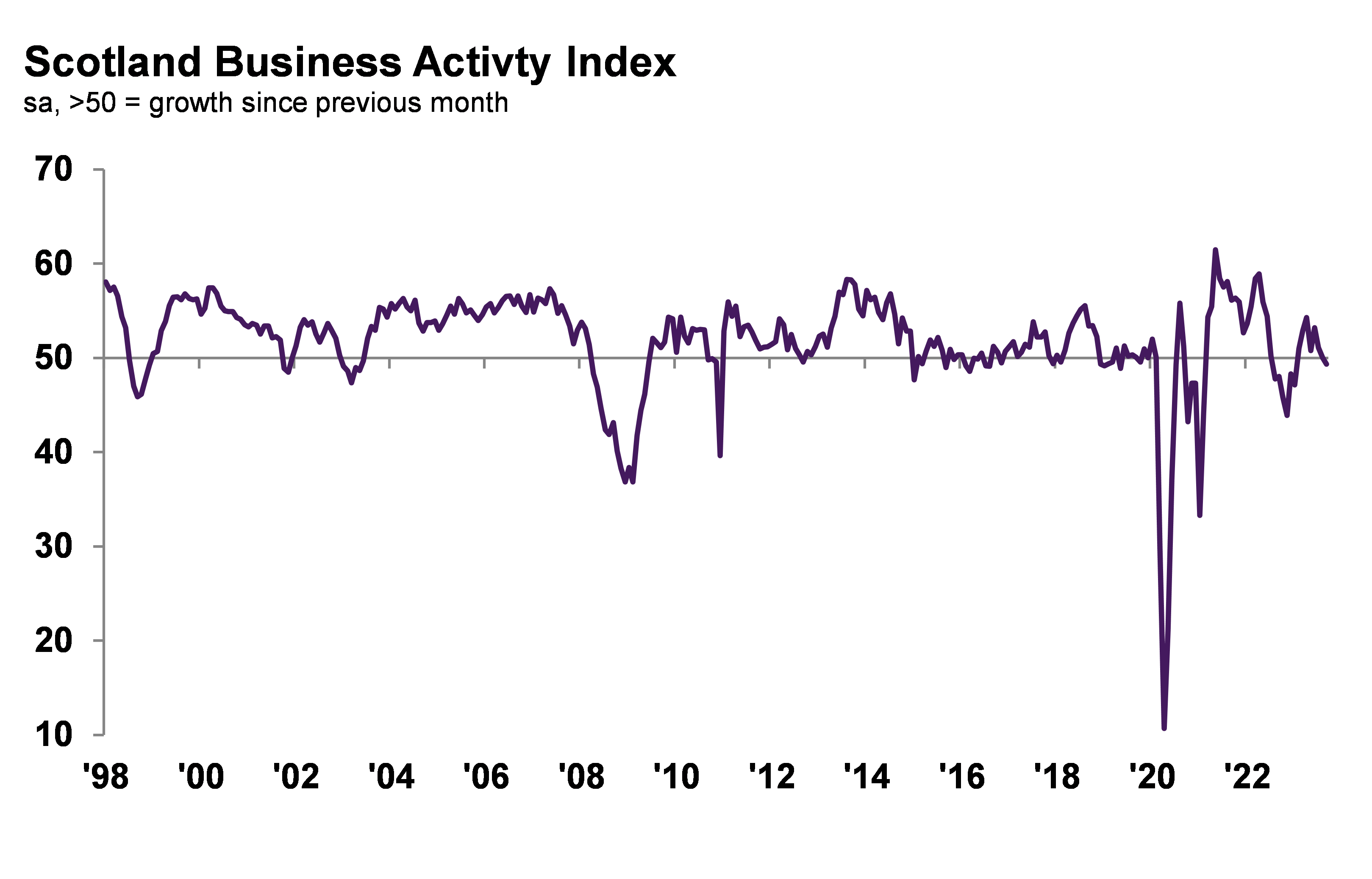

The Scotland Business Activity Index dropped to 49.3 from 50.0 in August, indicating a contraction. This was primarily attributed to a weakening in manufacturing and a downturn in services activity. However, this dip was marginal compared to the broader UK downturn, which stood at 48.5.

The downturn across Scotland reflected weakening demand conditions. Inflows of new work fell for the third consecutive month in September. Firms noted that general uncertainty shrouding the economic outlook and increased borrowing costs and inflationary pressures had squeezed disposable incomes, discouraging customer activity.

Scotland’s private sector recorded a further reduction in inflows of new work during September. According to anecdotal evidence, uncertainty surrounding the UK economic outlook and increased cost of living and borrowing costs weighed on customer demand. That said, the rate of decrease eased from August, with both sectors recording softer downturns.

New orders also fell across the UK as a whole, and at a stronger pace than that seen for Scotland.

Source: Royal Bank of Scotland, S&P Global PMl

Business confidence at Scottish private sector companies remained strong in September. Sentiment improved to a three-month high, with firms expecting growth in activity stemming from hopes of improved demand conditions, launch of new products and general market growth. Nonetheless, fears of increased competition and inflationary pressures resulting in fewer sales meant confidence levels remained historically muted.

Of the 12 monitored areas, only the North East and Northern Ireland recorded weaker sentiment than Scotland.

An eighth monthly expansion in employment was recorded across Scotland’s private sector in September. Panellists mentioned raising payroll numbers to return to pre-COVID levels. However, underlying data showed that job creation was limited to the service sector and was marginal overall.

Nonetheless, Scotland went against the broader UK trend. Northern Ireland also registered growth in jobs, but Wales and all nine English regions posted declines.

The level of unfinished work fell across Scotland’s private sector during September, with a contraction noted for the fifth month running. Firms mentioned that reduced order volumes and falling demand allowed companies to work through backlogs. However, the rate of depletion was modest overall and was outpaced by the UK trend.

Input prices continued to rise across Scottish private sector markets during September. Surveyed businesses often blamed growing cost burdens on wage inflation and material cost increases. Though marked and strong in context of the historical data, the rate of input price inflation moderated to a 31-month low, with both sectors reporting easing cost pressures.

The pace of input price inflation across Scotland was stronger than the UK average.

Average prices charged for the provision of private sector goods and services rose in Scotland during September. The respective seasonally adjusted index ticked up from August’s recent low and signalled a sharp increase in output charges. Higher cost burdens fed through to greater charges, panellists noted.

Furthermore, the output charge inflation across Scotland was sharper than the UK trend.

Judith Cruickshank

Judith Cruickshank, chair of RBS’ Scotland Board commented: “The third quarter ended with a fresh contraction in business activity across Scotland’s private sector, thereby marking the first fall in output since the start of the year.

“The downturn in activity was unsurprising as indicated by falling demand for Scottish goods and services for the third successive month in September.

“This, coupled with historically muted expectations for the outlook for output, signals a weak fourth quarter.”

She continued: “Whether the downturn will gain momentum or if demand trends can be reversed will be something to watch for in the coming months.

“In some positive news, cost burdens rose at the weakest pace in over two-and-a-half years. Cooler price pressures should eventually lead to renewed demand.”