ICAS tax experts share views on Scottish Budget

Justine Riccomini

The Institute of Chartered Accountants of Scotland’s (ICAS) experts have examined key aspects of the Scottish Budget announcement and how this addresses issues affecting many, such as the freezing of tax thresholds and increase in income tax.

On the key announcements in the Scottish Budget, Justine Riccomini, head of tax (employment and devolved taxes), said: “Today’s budget has not improved the tax burden on middle earners at a time of a cost-of-living crisis.

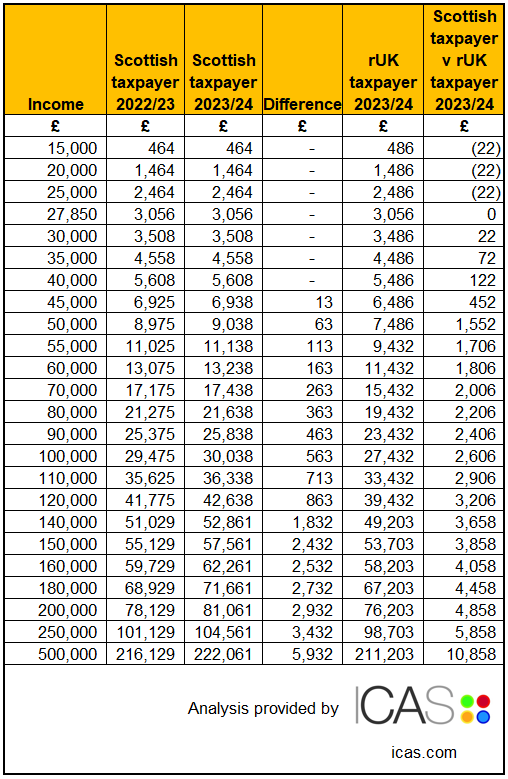

“With today’s Bank of England interest rate rise likely to impact mortgage payments, employees living in Scotland earning between £43,663 and £50,270 will now pay 42% Income Tax, as well as 12% Class 1 National Insurance, on each additional £1 they earn - which reflects an effective rate of tax of 54% in that earnings range - 22% more than their counterparts elsewhere in the UK.

“This is in stark contrast to Wales, which published its budget yesterday and once again chose to keep income tax rates and bands the same as those of Westminster.”

Scottish Rate of Income Tax (SRIT) - Additional rate band limit reduced from £150,000 to £125,140 in line with rest of UK

ICAS notes the reduction in the threshold for the top rate of income tax in Scotland to £125,140. As this is in line with the rest of the UK, the threshold will apply for Scottish taxpayers on their non-savings, savings and dividend income.

Ms Riccomini said: “After last month’s UK Autumn Statement, the lowering of the threshold for the top rate of income tax in Scotland was widely expected.

“This move could raise about £80 million, although the interactions with the Block Grant mechanism (Barnett Formula) under the Fiscal Framework agreement will essentially make this additional funding less visible, as they will be absorbed into a myriad of additional funding arrangements through the Block Grant.

“Had the Deputy First Minister chosen to do nothing, the Block Grant would have been augmented by around £1.5bn anyway.”

Chris Campbell

Chris Campbell, head of tax (tax practice and owner managed business taxes) at ICAS, said: “The reduction in the additional rate threshold will affect the Income Tax paid by successful unincorporated businesses. Many of those businesses may now wish to set up as a limited company, although this will be based on many different factors.”

Increase in top rate of SRIT from 46% to 47%

ICAS notes with concern the increase in the higher and top rate of income tax bands.

Ms Riccomini said: “Combined with the reduction in the top rate threshold, the increase in the higher rate and top rates of Income Tax could affect the attractiveness of Scotland as a place to set up a business.

“In many sectors, the international demand for talent means that salaries above £43,662, at which higher rate tax is paid, are not exceptional. The Scottish tax rate may make it more difficult to attract skilled workers to be employed in Scotland.”

“The combination of the 2% differential in both higher rate and top rate taxes between Scotland and the rest of the UK, together with the lower threshold at which higher rate tax starts in Scotland, may start to have an impact on people’s choices, particularly at middle income levels.”

Mr Campbell added: “The decisions on Scottish Income Tax rates will affect many Owner Managed Businesses based in Scotland. They may wish to consider whether to relocate elsewhere or set up as a limited company, although this is something they should seek professional advice on.”

SRIT - freezing of threshold rates

ICAS notes the freezing of the thresholds for the Scottish Rates of Income Tax.

Ms Riccomini commented: “Today’s Budget has not improved the tax burden on middle earners. Employees living in Scotland earning between £43,663 and £50,270 will be asked to pay 42% Income Tax, which is 22% higher than similar employees elsewhere in the UK. By freezing the tax bands, as wages rise, more and more employees will fall into this range.

This group of employees includes for example NHS Band 7 staff, which would include registered nurses, physiotherapists and mental health specialists. Attracting employees in this group to employers in Scotland becomes much more challenging with such a high marginal tax rate.”

Mr Campbell said: “Many family businesses who are sole traders or partnerships will have to pay additional Income Tax as a result of this change. In some cases, it could act as a disincentive for them to expand or grow their business.”

Land and Buildings Transaction Tax (LBTT) - increase in additional dwelling supplement rate from 4%

ICAS notes the increase in the rate of the Additional Dwelling Supplement (ADS) rate from 4% to 6%, effective from 16 December 2022.

Ms Riccomini added: “Whilst the ADS is ostensibly intended to improve the availability of housing for first time buyers, it is likely to be perceived by many as a ‘tax grab’, making it more expensive for those looking to buy a property to invest as an alternative source of income.”

Mr Campbell continued: “Companies buying residential property pay the Additional Dwelling Supplement on any purchase of residential property in Scotland above the £40,000 threshold, so this change will make it cost more for all companies in terms of the tax they pay on their residential property purchases in Scotland.”

LBTT - freezing of threshold rates

Ms Riccomini said: “The freezing of LBTT threshold rates is a stealthier way to raise tax across all society levels in Scotland. With mortgage interest rates expected to rise again following today’s Bank of England base rate announcement, it remains to be seen what the longer-term impact is on residential property transactions.

“The tax raising impact might be lower than expected if the property market sees significant reductions in volume or impacts on property prices.”

Increase in income tax by 1% to be ring fenced for health and social care

Ms Riccomini noted: “The Scottish Government has taken the unusual step of effectively substantially replacing the health and social care levy which was repealed by the UK Government in September 2022, by increasing income tax on the higher and top rate bands by 1% and ring-fencing it for health and social care.

“ICAS is not in favour of hypothecation and time will tell as to whether the taxpayers affected by the measure receive this well.”

Non-domestic rates

ICAS welcomes the extension of freezing of the Basic Property Rate of Non-Domestic Rates, as well as the incentives being given to businesses for investing in plant and machinery which will help facilitate the transition to Net Zero.

Mr Campbell said: “Businesses in Scotland were badly affected by the COVID19 pandemic, but may also be affected in the months ahead by reduced consumer demand amidst the cost of living crisis.

“Protection from inflation in Non-Domestic rates will be welcome for businesses as they navigate through a period of uncertainty, with smaller businesses also to benefit from the extension of the Small Business Bonus Scheme.

“We also welcome the announcement that the Scottish Government will encourage businesses to invest in renewable energy by granting exemptions from their Non-Domestic rates liability for purchasing qualifying plant and machinery. Our Members often tells us how tax reliefs will influence the right behaviour, so this is an excellent example of that.”

Scottish Landfill Tax - increase in rates

Ms Riccomini said: “Scottish Landfill Tax raises around £100m per annum for the Scottish Government and the increase in rates payable will not significantly impact the Scottish Government’s budget income.

“We however welcome the increase, as it is expected that it will contribute towards a more sustainable Scotland and encourage positive direction of travel in the drive towards Net Zero.”

Measures not announced

David Menzies, director of practice, noted: “It is unfortunate that the Deputy First Minister did not indicate in his Statement any movement on the devolved tax powers in relation to VAT and Air Departure Tax.

“Both powers have now been available to the Scottish Government for several years but issues on their introduction remain unresolved. ICAS would like to see a clear path set out for both measures to assist in providing business with certainty over their introduction - or that the powers will not be used.”